The purchased goods would be recorded on the buyer’s balance sheet at this point. If the freight classification is FOB destination, then the seller records the transportation cost as freight-out, transportation-out or delivery expense. FOB destination requires a debit to freight-in and a credit to accounts payable. Sellers – who pay freight under FOB shipping point – debit delivery expense while crediting accounts payable.

The Metro company uses net price method to record the purchase of inventory. All that said, many general accounting departments still struggle with how and when to record freight costs and get blamed for not doing things correctly. But having an accounting department sifting through freight expenses to decide which is freight in and freight out is not a good operational practice. Merchandise Inventory increases (debit) and Accounts Payable increases (credit) by the amount of the purchase, including all shipping, insurance, taxes, and fees [(40 × $60) + (40 × $5)].

Delivery of goods example

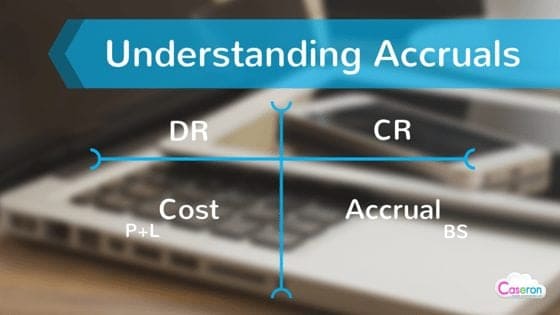

Accrued freight is the expenses incurred but not paid, and the liability payment is deferred to another date. As per the Accrual basis of accounting, we need to accrue all the expenses relating to the respective year. Total assets on the balance sheet declined by $200, while expenses on the income statement increased by the same amount in this journal entry. Freight-out or delivery expenses generally serve the same purpose and are similar.

- The point of transfer is when the goods leave the seller’s place of business.

- The cost principle requires this expense to stay with the merchandise as it is part of getting the item ready for sale from the buyer’s perspective.

- The provider charges ₹60 to send the items by Federal Delivery Company.

- As we do not update inventory immediately upon purchase under the periodic inventory system, we cannot include the freight-in cost immediately to the cost of inventory.

The Sum of sales returns they subtract from the company’s overall sales. Upon that debit section of the balance sheet, return inwards is where the negative amount is kept. You are a seller and conduct business with several customers who purchase your goods on credit. Your standard contract requires an FOB Shipping Point term, leaving the buyer with the responsibility for goods in transit and shipping charges. One of your long-term customers asks if you can change the terms to FOB Destination to help them save money.

Want better grades, but can’t afford to pay for Numerade?

Let us below understand the definition of carriage inwards and carriage outwards meaning in detail. You need to keep track of how and why you’re paying for the freight costs. If you’re buying inventory, for example, the supplier might charge you for the freight. That freight cost would go into a freight account that is incorporated free file fillable forms into your cost of goods. IFRS allows greater flexibility in the presentation of financial statements, including the income statement. Under IFRS, expenses can be reported in the income statement either by nature (for example, rent, salaries, depreciation) or by function (such as COGS or Selling and Administrative).

Let’s say a vendor sells ₹800 worth of goods with the phrases FOB Location. The provider charges ₹60 to send the items by Federal Delivery Company. Transactions of ₹800 will be shown on the provider’s financial statements. It will also include a ₹60 operational expense for carriage outside (or delivering cost). These days, company operations span both nationwide and global boundaries. Corporate entities frequently use inputs originating from several geographic places to manufacture their products and services.

We use the periodic inventory system to manage the merchandise inventory in our company and the $5,000 merchandise goods arrive at our place on the same day of purchase. For example, on February 1, we make a cash purchase of $5,000 merchandise goods from one of our suppliers. In addition to the purchase amount, we also pay $200 in cash for the delivery cost in order to bring the merchandise goods to our office. Freight is the shipping charge for transporting inventory, either purchases or sales. If suppliers are liable for the cost, they must report an operating expense, whereas customers may be able to include the cost in the Cost of Goods Sold (COGS).

Discussion and Application of FOB Destination

In this instance, they consider internal transportation as a buy cost. Keep in mind that when these commodities are sold, the price of inbound transportation and the initial price are part of the revenue comments of Cost of Goods Sold. The return of goods from customers to seller also involves two journal entries – one to record the sales returns and allowances and one to reverse the transfer of cost from inventory to COGS account. If you don’t have a freight expense account, you should set one up in your chart of accounts.

In the examples above, the freight that you paid to have inventory or parts of inventory shipped to you, so freight-in, that would be part of the laid-down cost. They may not know whether it’s a part of an inventory buy or if it’s part of something that was shipped out to a customer. You need to push it downstream to that level of your operation to make sure that by the time it gets to accounting, there’s no doubt where it should go.

Paid freight journal entry

To illustrate, suppose CBS sells 30 landline telephones at $150 each on credit at a cost of $60 per phone. On the sales contract, FOB Destination is listed as the shipping terms, and shipping charges amount to $120, paid as cash directly to the delivery service. When you buy merchandise online, shipping charges are usually one of the negotiated terms of the sale. As a consumer, anytime the business pays for shipping, it is welcomed. For businesses, shipping charges bring both benefits and challenges, and the terms negotiated can have a significant impact on inventory operations. As we do not update inventory immediately upon purchase under the periodic inventory system, we cannot include the freight-in cost immediately to the cost of inventory.

Five ways AI is transforming the trucking industry – CCJ

Five ways AI is transforming the trucking industry.

Posted: Tue, 08 Aug 2023 07:00:00 GMT [source]

Because freight-out is a cost incurred by the firm to assist the sale of its goods, it is usually reported as an item in the income statement’s selling costs column. The purchase cost of products in this journal entry is separate from the freight-in journal entry. Like the purchase account, the freight-in account is a temporary account that will be cleared when the firm calculates the cost of goods after the accounting period. After all, the inventory account and cost of goods sold will only be updated when the firm takes a physical inventory count under the periodic inventory system (usually at the end of the period).

Cost of delivery goods out or freight out

Let us look into the carriage outwards, meaning the price of transportation borne by the supplier while selling items to the purchaser is known as carriage outwards. Carriage outbound refers to the transportation expenses spent whenever a seller sends products to a purchaser by a certain means of transportation. Carriage outwards is the name given to this expense because it occurs whenever products leave the company. The balance in inventory account at the end of an accounting period shows the cost of inventory in hand. The accuracy of this balance is periodically assured by a physical count – usually once a year. If a difference is found between the balance in inventory account and the physical count, it is corrected by making a suitable journal entry (illustrated by journal entry number 6 given below).

Lovesac to restate yearly, quarterly income figures following internal … – Furniture Today

Lovesac to restate yearly, quarterly income figures following internal ….

Posted: Fri, 18 Aug 2023 07:00:00 GMT [source]

Our review course offers a CPA study guide for each section but unlike other textbooks, ours comes in a visual format.

For example, the company ABC incurs the transportation cost of $100 when it makes the sale and delivers the goods to one of its customers. On the same day, Metro company pays $320 for freight and $100 for insurance. Both merchandising and manufacturing companies can benefit from perpetual inventory system.